Expecting Parents: Daycare is your New Large Expense

Insights Young ProfessionalBrennan McCarthy, CFP®

Every parent agrees that they’d do anything for their child(ren). Most of us spent months researching strollers, car seats, and nursery furniture as soon as we found out a baby is coming. We read every review, compare every model, and agonize over the right wall color for the baby’s room.

A lot fewer expecting parents put that same level of research into the cost of daycare. And their budgets are put under a lot more stress as soon as that big expense starts up.

What Infant Daycare Actually Costs

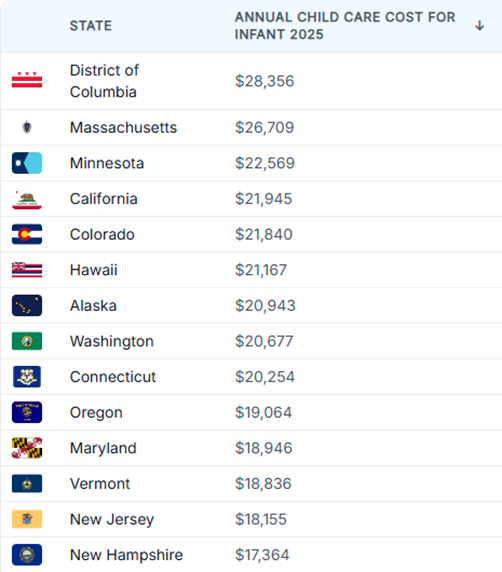

In the Twin Cities, full-time infant daycare typically runs anywhere from $1,300 to $2,000 per month. That's $15,600 to $24,000 per year — for one child. This isn't unique to Minnesota, but it is the 2nd highest cost state in the country (3rd, if you count Washington DC).

According to the Economic Policy Institute, the average annual cost of infant care exceeds the cost of in-state college tuition in most U.S. states. And unlike college, you don’t have 18-years to save and prepare for it. And good luck finding a “student loan” to pay for it.

For most dual-income households, daycare becomes the third-largest monthly expense — right behind the mortgage and health insurance. Many couples don't see it coming with that kind of force until it hits.

A Simple Strategy That Actually Works

I recently worked with a couple in their early 30s — both professionals, both earning solid incomes, generally on top of their finances. For the most part they were financially prepared for a baby in the broad sense.

But when we sat down and mapped out the full picture of what a newborn would cost them, adding in a $1,500/month expense turned their monthly cash flow upside down.

So we the same thing I tell all my clients in their situation. We set up a gameplan immediately. The day they let me know they were pregnant, we set up an automatic transfer of $1,500 per month into a dedicated money market account earmarked for childcare. It required us to tweak some of their other savings and temporarily reduce what they were saving in their 401(k)s, but the system was set up.

Nine months later, when their daughter arrived, they had an extra $9,000 in cash sitting there, ready to absorb those first several months of daycare bills. While they did have to adjust their lifestyle by a couple hundred dollars each month, they didn't have to cut anything dramatically. They had time to adjust to their new budget without the financial pressure hitting all at once.

Why Automation Is the Real Secret

I work with a lot of highly competent professionals, and the truth is, automating their savings creates a lot better outcomes in 90% of them. Even disciplined, high-earning people struggle to consistently set money aside when it requires a conscious decision every month. Unexpected expenses pop up, and the money that was "going to savings" ends up somewhere else.

Automating a transfer (either monthly or bi-weekly) removes the decision entirely. The money moves before you have a chance to spend it on something else — before the weekend trip, before the new gear purchase, before you even really notice it's gone.

This is the same principle behind 401(k) contributions: they work largely because they're invisible. You never see the money hit your checking account, so you don't miss it, and you don't spend it.

It’s a proven method, so there’s no reason to mess with what works. Set up the transfer the day you find out. Pick an amount that's slightly uncomfortable but manageable — somewhere in the range of what you expect to pay for daycare. Then leave it alone.

By the time your baby arrives, you won't have just saved a good chunk of money. You'll have built a habit of living without that portion of your income, which makes the actual daycare bill far less disruptive when it shows up.

How to Set This Up Today

If you're expecting — or even just starting to think about having a child — here's a practical framework:

- Research local daycare costs now. Don't wait. Call two or three centers in your area and ask for their infant room rates. Get a real number, not an estimate from a friend.

- Open a separate savings account. Keep this money out of your regular checking account. Label it something specific — "Daycare Fund" or "Baby Costs." Separation creates clarity and reduces temptation.

- Set up an automatic transfer the day you find out. Even if it's a smaller amount than the eventual daycare cost, start immediately. Every month counts.

- Adjust as you get further along. As your due date approaches and your expenses shift, revisit the transfer amount. The goal is to arrive at delivery with at least three to six months of daycare expenses already saved.

The Broader Lesson

Working with high earners has taught me that simple strategies are almost always better than complex ones, even when dealing with somebody with a complex financial life.

That's why automating savings works. It removes the decision-making power from your hands each month, and instead of forcing your willpower to make the right choice every time, you just have to make that decision once and leave it alone.

If you're an expecting parent, the sooner you start this process, the better off you’ll be. The longer you wait, the more painful it will feel when the daycare fees start hitting your bank account.