The Hidden Cost of Roth Conversions (and When to Actually Do one)

Investing Retirement Funding Insights Young ProfessionalBrennan McCarthy, CFP®

Imagine writing a $35,000 check to the IRS that you didn’t have to write – and calling it a good financial decision. That is exactly what I’ve seen from some high earners completing Roth Conversions in the same year they earned $300,000 (or more).

The concept of Roth Conversions is great: pay tax on the seed today so you don’t have to pay tax on the harvest later. The problem is it neglects the most important reason for doing Roth Conversions: Tax Arbitrage. In other words, can I reasonably expect that by doing this Roth conversion today (and pre-paying the taxes today), the total tax bill will be lower today than in the future?

What is a Roth Conversion?

At its simplest, a Roth conversion is the process of moving money from a "pre-tax" retirement account (like a Traditional 401(k) or Traditional IRA) into a Roth IRA.

When you contributed to your 401(k) or IRA originally, you likely received a tax deduction—the IRS let you "skip" paying taxes on that income in the year you made the contribution, so it could grow for your future. Because you got a tax benefit to put money into the account, a withdrawal from the account means the full amount will get taxed at your personal income tax rate. A Roth conversion is essentially telling the IRS that you’re ready to pay that tax bill now.

The mechanics are straightforward:

- The Conversion: You move a specific dollar amount from your pre-tax account to a Roth IRA.

- The Tax Bill: The amount you move is added to your taxable income for the year. If you convert $50,000, the IRS treats it as if you earned an extra $50,000 in salary.

IMPORTANT: Since the goal of this strategy is to get as much into the Roth environment as possible, you will NOT want to withhold taxes on the conversion. You will get the most impact out of this strategy if instead, you pay the tax bill out of pocket (or from taxable brokerage account investments).

- The Reward: Once that money is inside the Roth, it never faces the IRS again. Every dollar of future growth and every withdrawal you make in retirement is 100% tax-free.

We all want to pay tax on the smaller amount (seed) today so we can avoid paying tax on the bigger amount (harvest) later, but this metaphor misses the logic that taxing 35% (or more) of the seed is costlier than paying 10% or 12% of the harvest later in retirement.

Why Your Peak Earning Years Are Probably the Worst Time for a Roth Conversion

There are a handful of scenarios where doing a Roth conversion is a great strategy, but more situations where doing it would severely set you back.

The reality is that a Roth conversion isn't a magic tax-evasion tool; it’s a tax-prepayment strategy. And you generally don't want to prepay a bill when it's at its all-time high.

The Math of "Tax Arbitrage"

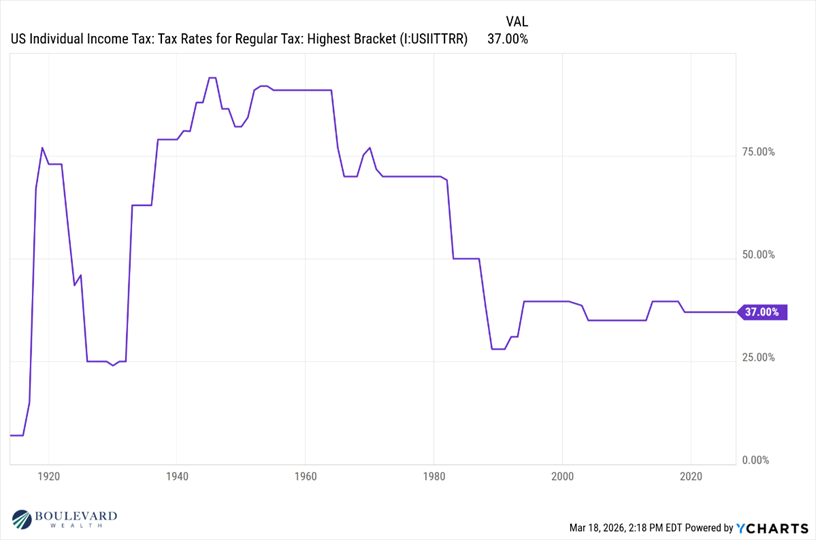

The success of a Roth conversion relies almost entirely on tax arbitrage—the difference between the tax rate you pay today versus the tax rate you will pay in the future.

- Scenario A: You convert now while in the 32% or 35% federal bracket.

- Scenario B: You wait until retirement when your "earned income" drops to zero, potentially falling into the 12% or 22% bracket, and convert then.

By converting during your high-income years, you are essentially "buying" tax-free growth at a 32-cent premium. If you wait until your income drops in retirement, you could buy that same tax-free growth for 12 or 22 cents.

Three Reasons to Wait for the "Trough Years"

Most of my clients find their best conversion opportunities during the "Trough Years"—the window after you retire but before you start Social Security and Required Minimum Distributions (RMDs). Here is why waiting usually wins:

1. The "Bracket Bump" Trap

When you convert $100,000, that amount is added to your taxable income for the year. If you’re already a high earner, that $100,000 is taxed at your highest marginal rate. It might even push you into a higher bracket or trigger the Net Investment Income Tax (NIIT), making the conversion even more "expensive" than you anticipated.

2. Paying the "Devil You Know" Too Early

As the Federal deficit continues to balloon year after year, experts conclude that our tab is going to come due, so tax rates will rise over the next decades. With that said, these same “experts” have also been saying the same thing for the past 50 years, and rates have only decreased since then. The speculative nature of future tax rates is exactly why you should only focus on what’s knowable (your current vs. projected retirement income), rather than gambling on what our politicians will decide.

3. Opportunity Cost of the Tax Payment

To make a conversion work, you should ideally pay the taxes using "outside" cash (like a brokerage account), not from the IRA itself. If you write a $35,000 check to the IRS today to convert $100,000, that $35,000 is no longer invested and growing for you. You need the Roth's tax-free growth to outperform the lost growth on that $35,000—a hurdle that is much harder to clear when your initial tax bill is high.

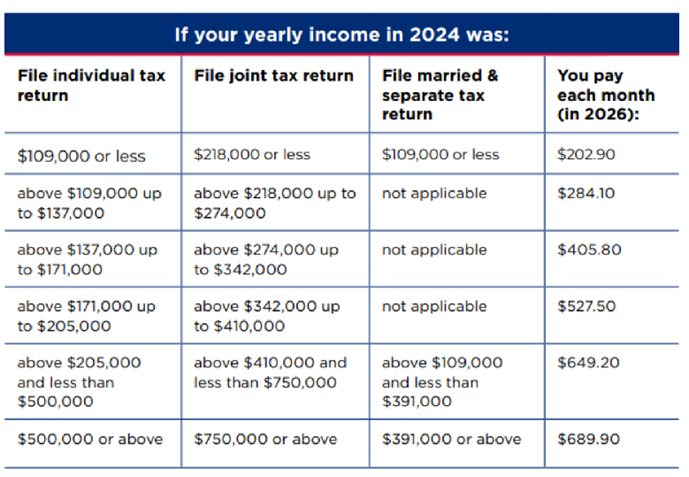

The Biggest Pitfall: The IRMAA Cliff

When you’re 63 or older, a Roth conversion comes with a secondary "tax" that most people don’t see coming until two years later: IRMAA (Income-Related Monthly Adjustment Amount).

If your income exceeds certain thresholds ($218,000 for a married couple), the government adds a surcharge to your Part B and Part D premiums. Because Medicare uses a two-year look-back period, a conversion you do today in 2026 will dictate what you pay for healthcare in 2028.

A conversion pushing a married couple even $1 over the income threshold could cost thousands in Medicare surcharges, and you probably won’t learn about it until 2 years down the road.

Table provided by www.medicare.gov/publications/11579-medicare-costs.pdf

If your conversion pushes you just slightly over these marks—or any of the four higher tiers above them—you aren't just paying more in income tax; you are effectively paying a "healthcare surcharge" that can significantly eat into the long-term benefits of the Roth.

When Does a Conversion during Working Years Make Sense?

For the majority of pre-retirees, it doesn’t make sense to do a Roth conversion while you’re working. However, when it comes to financial planning, there are always exceptions:

A Large Business Loss: If you own a business and experience a significant loss in a given year, that loss can offset your ordinary income — temporarily dropping you into a much lower bracket than usual. Consider a business owner who normally earns $300,000 but reports a $200,000 operating loss in a restructuring year, bringing their taxable income down to $100,000. That window could be an ideal time to convert, because you're paying taxes on that Roth conversion at a fraction of your normal tax rate.

A Sabbatical or Career Transition: Taking a year off between jobs, stepping back to part-time work, or simply in a commission-based role with a lower-than-normal income year. A dual-income couple where one spouse leaves their $150,000 job in March, for example, might find their combined taxable income for that year is 40-50% lower than normal — a meaningful opportunity to convert at a lower rate before income returns to its usual level.

A Significant Market Downturn: When markets drop sharply, your pre-tax retirement account balance temporarily shrinks — meaning you can convert the same number of shares for a lower taxable dollar amount. If your Traditional IRA dropped from $1,000,000 to $700,000 during a correction, converting a portion now means you're paying taxes on the depressed value, and all of the subsequent recovery happens inside the tax-free Roth environment. This is one of the few times where a bear market is working in your favor.

The Bottom Line

Roth conversions are a powerful tool, but they are a surgical instrument, not a sledgehammer. In my experience, the best Roth conversion strategy often means doing nothing until the moment is exactly right.